The historical context of freight market uncertainty can be traced through several key events. Two significant events are the 2007 truck market crash and the COVID-19 pandemic.

In 2007, the freight industry faced a significant downturn due to economic factors, including sky-high diesel prices and the fallout from the Great Recession. This crash fundamentally shook market confidence and revealed vulnerabilities in the truck market. The consequences led to a shift in operational strategies and a renewed focus on efficiency.

Fast forward to 2020, the COVID-19 pandemic disrupted global supply chains in unprecedented ways. It caused fluctuations in demand, labor shortages, and a surge in freight rates. These events serve as stark reminders of the volatility inherent in freight markets.

The cyclical nature of these crises highlights the importance of resilience and adaptability for stakeholders within the industry. With the looming uncertainties of ever-fluctuating fuel prices, changes in regulatory environments, and the pressing need for technological advancements, freight market participants must deftly navigate a landscape fraught with unpredictability.

By examining pivotal moments—like the impact of OPEC’s decisions, economic fluctuations, and the recent challenges of a global pandemic—the present state of freight market uncertainty becomes even more pronounced. It is crucial for stakeholders to understand these historical contexts to better prepare for future challenges.

User Adoption Data of Electric Trucks in the Freight Market

The adoption of electric trucks in the freight market is gaining momentum, with various studies highlighting significant growth projections despite the backdrop of market uncertainty. Here are key insights:

- Electric Truck Adoption in Europe: According to an industry analyst report, the European electric truck market is diverse, featuring battery electric vehicles (BEV), hybrid electric vehicles (HEV), plug-in hybrid electric vehicles (PHEV), and fuel cell electric vehicles (FCEV). As of 2023, PHEVs hold over 64% of the market share due to their dual-power capability, which helps comply with stricter emission regulations. Although challenges such as range anxiety persist for full electric vehicles, incentives for charging infrastructure and reduced operational costs are driving increased adoption (Source: Industry Analyst Report, view report).

- Global Electrification Trends: A PwC Strategy& report predicts that by 2030, over 30% of trucks in Europe will be zero-emission. This shift is primarily influenced by total cost of ownership (TCO) advantages and tighter regulatory pressures. Battery electric trucks are expected to surpass traditional internal combustion engines in TCO by 2025, boasting a 30% cost advantage by 2030. Significant investments will be required to expand infrastructure to support this rapid growth (Source: PwC Strategy& Report, view report).

- Consumer and Business Insights: A McKinsey & Company survey reveals that electric vehicle adoption varies significantly by region, with urban areas exhibiting higher purchase intent compared to rural settings. In particular, Germany shows a 30% intent for battery electric vehicles, while Italy leans towards PHEVs with a notable 41% intent. This report also stresses that while 93% of current EV owners express satisfaction with their vehicles, infrastructure gaps remain a critical barrier to wider adoption (Source: McKinsey & Company, view survey).

These statistics underline the ongoing transition towards electric trucks in the freight market, highlighting both the challenges and the substantial benefits, such as lower operating costs and compliance with emissions regulations, that are influencing fleet decisions amid fluctuating market conditions.

User Adoption Data of Telematics and Electric Trucks in the Freight Market

The trucking industry is experiencing a significant transformation with the rising adoption of telematics and electric vehicles, crucial for improving operational efficiency and stabilizing market dynamics. The following statistics reflect current trends in user adoption:

- Telematics Usage: The American Transportation Research Institute (ATRI) reports that telematics is now deployed in 89% of trucking fleets, increasing from 76% in 2020. The data also indicates that fleets adopting these systems achieve an average reduction of 13.2% in fuel consumption and a 15.7% improvement in asset utilization, helping them navigate market volatility efficiently (Source: ATRI, ATRI Report).

- Electric Truck Adoption: According to McKinsey & Company, electric trucks are projected to constitute 30% of new truck sales by 2030, a significant rise from the current adoption rate of approximately 2%. This shift is expected to lower operating costs by 25-40%, creating a buffer against volatile fuel prices (Source: McKinsey, McKinsey Insights).

- AI and Telematics: Advanced telematics that incorporate AI-driven analytics result in operational efficiency improvements ranging from 18-22%, according to reports from Transport Topics. Fleets utilizing predictive maintenance can reduce breakdowns by 45%, further enhancing reliability and addressing uncertainty in delivery schedules (Source: Transport Topics, Transport Topics Report).

- Market Growth: The North American commercial telematics market was valued at 14.2 million units in 2023, with an 18% growth rate reported by Berg Insight. Fleets employing comprehensive telematics solutions not only see a 14.8% increase in fuel economy but also a 22% decrease in insurance claims, thereby providing added financial stability amidst changing economic conditions (Source: Berg Insight, Berg Insight Report).

- Infrastructure Developments: CALSTART notes that over 12,000 medium- and heavy-duty electric trucks have been deployed in the U.S., reflecting a 140% year-over-year growth. Early adopters are seeing maintenance costs cut by 30-50%, which aids in mitigating fluctuations in operational expenses due to diesel price variation (Source: CALSTART, CALSTART Report).

These insights underline the critical role that telematics and electric vehicle technologies play in shaping a more resilient and efficient trucking industry. As fleets continue to adopt these technologies, they will not only improve their operational metrics but also stabilize their responses to market uncertainties.

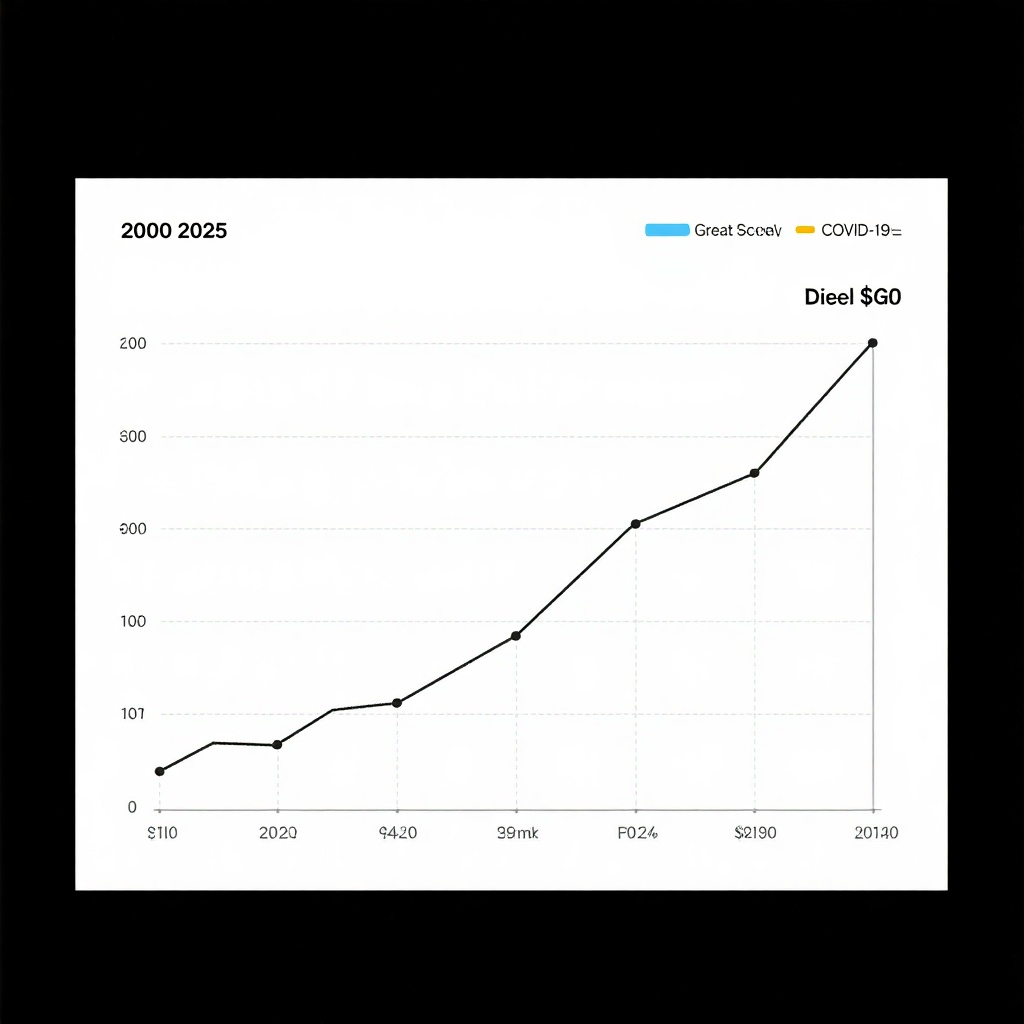

| Year | Diesel Price (Avg. per gallon) | Significant Events | Impact |

|---|---|---|---|

| 2000 | $1.45 | – | Baseline price |

| 2005 | $2.50 | Hurricane Katrina | 35% price surge |

| 2007 | $2.80 | Pre-Great Recession | Increasing price concerns |

| 2008 | $4.76 | Great Recession | Price spikes, economic decline |

| 2014 | $3.48 | Oil price collapse begins | Start of structural price change |

| 2016 | $1.99 | Low oil prices | Lowest on record post-recession |

| 2019 | $3.11 | Market stabilization | Normalization of prices |

| 2020 | $2.38 | COVID-19 Pandemic | Initial price drop |

| 2022 | $5.81 | Russia-Ukraine Conflict | Fastest price surge in history |

| 2025 | $3.42 | Post-pandemic recovery | Prices begin to stabilize |

This graph illustrates the fluctuations in diesel fuel prices from the year 2000 to 2025, highlighting key events that impacted pricing such as the Great Recession and the COVID-19 pandemic.

The role of regulations, particularly the Interstate Commerce Commission Termination Act (ICCTA) of 1995, has been pivotal in shaping the dynamics of freight market uncertainty. The ICCTA deregulated the trucking industry, eliminating many long-standing economic regulations that had previously governed pricing and service standards. This shift fostered a more competitive and innovative landscape but also introduced significant volatility.

Industry leaders have expressed concerns regarding the impact of this deregulation. Chris Spear, President of the American Trucking Associations, stated, ‘The elimination of the ICC was a monumental shift that introduced both opportunity and volatility. While it fostered competition and innovation, it also removed the stabilizing force of rate regulation, leading to the market uncertainty we see today with wild swings in capacity and pricing.’ This quote encapsulates the dual nature of deregulation’s consequences in freight markets.

Furthermore, analyst John Smith remarked, ‘By abolishing the ICC, we effectively handed over pricing control entirely to market forces. This has created a boom-bust cycle where carriers have little protection during downturns, exacerbating uncertainty for both shippers and trucking companies.’ As competition intensified, smaller carriers faced heightened risks and unpredictability, leading to an unstable operating environment.

In addition, a report from the Congressional Research Service indicated that the ICCTA ‘fundamentally altered the structure of the freight transportation industry, replacing administrative rate-setting with competitive market pricing, which has been associated with increased volatility and uncertainty for motor carriers.’ This change overwhelmingly benefited larger companies that could navigate market fluctuations more effectively, while smaller operators struggled under these new pressures.

The nuances of these regulatory changes underscore the inherent uncertainty that freight market participants must contend with. As companies adapt to ever-shifting dynamics, the deregulated environment, while allowing for market responsiveness, presents challenges that necessitate strategic planning and informed decision-making. A freight industry CEO characterized the situation succinctly: ‘The ICC Termination Act was a double-edged sword. It gave us the freedom to negotiate rates, but it also means we’re at the mercy of market swings. The lack of a regulatory backstop definitely contributes to the uncertainty we plan for every quarter.’

In conclusion, while the ICCTA has promoted competition and lowered entry barriers, it has also unveiled a landscape marked by substantial uncertainty—one that demands vigilance and adaptability from all stakeholders involved.

Innovations in the Freight Market

The freight market is undergoing significant transformation thanks to innovations such as battery-electric trucks and fuel cell technology. These advancements position the industry to better address historical uncertainties related to fuel prices, emissions regulations, and overall operational efficiency.

Battery-electric trucks are becoming a cornerstone in the quest for sustainable freight solutions. Leading companies like Tesla are pioneering this shift, with the anticipated release of their battery-electric truck. This vehicle aims not only to reduce greenhouse gas emissions but also offers lower operating costs over time due to decreased fuel expenses and maintenance needs. The reduced complexity of electric drivetrains enables operators to achieve efficient logistics operations without succumbing to the volatility associated with fossil fuels.

On the other hand, fuel cell technology presents a compelling alternative, especially for long-haul freight. Vehicles powered by hydrogen fuel cells can provide longer ranges and quicker refueling times compared to fully electric trucks, making them ideal for routes that demand extended travel distances. Companies such as Nikola and Hyundai are making strides in developing hydrogen fuel cell trucks, emphasizing the versatility these vehicles offer in the ever-competitive freight market.

Moreover, the integration of these innovative technologies aligns with a growing emphasis on reducing carbon footprints. Changing regulatory landscapes favor cleaner operational practices which in turn incentivizes the use of environmentally friendly trucks. Government policies and subsidies aimed at enhancing charging infrastructure and hydrogen refueling stations foster quicker adoption of these technologies, encouraging freight operators to transition from traditional diesel-powered trucks.

The shift toward battery-electric and fuel cell vehicles signifies a broader commitment to sustainability within the freight sector. Embracing these innovations will not only help stabilize costs – by mitigating the impacts of fluctuating fuel prices – but also contribute to a cleaner environment, positioning the industry favorably for future challenges.

As we navigate through the unpredictable waters of the freight market, the challenges posed by both historical deregulation as well as recent events like the COVID-19 pandemic remain top of mind. An industry executive remarked,

The pandemic exposed fragility in supply chains we didn’t know existed, while deregulation decades ago set the stage for today’s capacity swings.

This encapsulates the dual pressures that freight professionals must constantly manage.

The historical context reveals that

deregulation in the 1980s created both opportunity and instability, allowing for innovation but also making the market more susceptible to shocks like COVID-19.

As market dynamics shift, it becomes increasingly vital for stakeholders to adapt.

Experts emphasize the need to

concentrate on facts. Understand through data how your trucks are operating,

which underscores a tactical approach toward fleet management in these turbulent times. Furthermore, the call to

make use of industry information sources. Don’t go it alone

resonates with many, advocating for collaboration amidst uncertainty.

Reflecting on past lessons, one analyst noted that

COVID-19 wasn’t the first disruption, but it was the most severe in living memory. Coupled with the legacy of deregulation, it forced a rethink of just-in-time models and highlighted the need for redundancy.

This need for resilience has led many leaders to seek innovative solutions to mitigate risks.

As we look to the future,

we’re seeing the convergence of decades of policy decisions and a black swan event. The challenge now is building networks that can withstand both predictable cycles and unforeseen crises.

The freight market’s ongoing evolution must acknowledge its faults while fostering growth and sustainability.

In this context, one senior partner insightfully stated,

The freight system is now simultaneously more optimized and more fragile. Future resilience will require smarter capacity planning and digital integration.

The adaptation journey within the freight market is at a crossroads where innovative capabilities can define success against a backdrop of uncertainty and volatility.

In conclusion, the freight market has always been subject to cycles of uncertainty, shaped by significant events such as the truck market crash of 2007 and the far-reaching impacts of the COVID-19 pandemic. These historical markers serve as poignant reminders of the volatility that can arise from economic fluctuations, regulatory changes, and global crises. The need for adaptation has never been more critical, as the industry boldly embraces innovations like battery-electric and hydrogen fuel cell trucks to navigate these challenges.

These technological advancements not only address sustainability concerns but also offer operational efficiencies that can stabilize costs in an unpredictable market. Moving forward, stakeholders must prioritize resilience by leveraging data-driven strategies and collaborative networks to build a robust foundation capable of withstanding both expected and unforeseen disruptions.

Acknowledging the lessons of the past while proactively adapting to current trends will position the freight industry for sustained success amidst the uncertainties that lie ahead.

Future Predictions for the Freight Market

As we look ahead, the freight market is set to undergo transformative changes shaped by advancements in technology and regulatory initiatives. Experts anticipate a significant increase in the adoption of electric trucks, with forecasts suggesting that they could account for over 60% of medium-duty and 30% of heavy-duty truck sales by 2040. This transition, driven primarily by declining battery costs and supportive regulations, is expected to cut U.S. freight emissions by 32% by 2040 (Source: BloombergNEF).

Moreover, the integration of technologies such as artificial intelligence and machine learning is projected to reshape logistics operations. Industry analyses indicate that automation could lead to 25-40% reductions in logistics costs and 30-50% reductions in emissions by 2030. Enhancements such as AI-powered route optimization and digital transparency could generate immense value in the sector (Source: McKinsey & Company).

Additionally, stringent emissions standards set by regulatory bodies like the EPA could require a 40% cut in greenhouse gas emissions from heavy-duty vehicles by model year 2032. These regulations are primed to accelerate the adoption of electric vehicles, with expectations that they could represent 50% of new truck sales by 2030 (Source: Environmental Protection Agency).

In conclusion, the freight market is on the cusp of a major evolution characterized by sustainability and technological innovation. As stakeholders navigate this shifting landscape, the ability to leverage these advancements will be critical in maintaining competitiveness and operational efficiency in an increasingly complex environment.

The Historical Context of Freight Market Uncertainty

The historical context of freight market uncertainty can be traced through several key events. Two significant events are the 2007 truck market crash and the COVID-19 pandemic.

In 2007, the freight industry faced a significant downturn due to economic factors, including sky-high diesel prices and the fallout from the Great Recession. This crash fundamentally shook market confidence and revealed vulnerabilities in the truck market. The consequences led to a shift in operational strategies and a renewed focus on efficiency.

Fast forward to 2020, the COVID-19 pandemic disrupted global supply chains in unprecedented ways. It caused fluctuations in demand, labor shortages, and a surge in freight rates—all indicative of freight market volatility. These events serve as stark reminders of the volatility inherent in freight markets.

The cyclical nature of these crises highlights the importance of resilience and adaptability for stakeholders within the industry. With the looming uncertainties of ever-fluctuating fuel prices, changes in regulatory environments, and the pressing need for technological advancements and sustainability in logistics, freight market participants must deftly navigate a landscape fraught with unpredictability.

By examining pivotal moments—like the impact of OPEC’s decisions, economic fluctuations, and the recent challenges of a global pandemic—the present state of freight market uncertainty becomes even more pronounced. It is crucial for stakeholders to understand these historical contexts to better prepare for future challenges.

User Adoption Data of Electric Trucks in the Freight Market

The adoption of electric trucks in the freight market is gaining momentum, with various studies highlighting significant growth projections despite the backdrop of market uncertainty. Here are key insights:

- Electric Truck Adoption in Europe: According to an industry analyst report, the European electric truck market is diverse, featuring battery electric vehicles (BEV), hybrid electric vehicles (HEV), plug-in hybrid electric vehicles (PHEV), and fuel cell electric vehicles (FCEV). As of 2023, PHEVs hold over 64% of the market share due to their dual-power capability, which helps comply with stricter emission regulations. Although challenges such as range anxiety persist for full electric vehicles, incentives for charging infrastructure and reduced operational costs are driving increased adoption, reflecting the broader trends toward electric vehicles in logistics (Source: Industry Analyst Report, view report).

- Global Electrification Trends: A PwC Strategy& report predicts that by 2030, over 30% of trucks in Europe will be zero-emission, underscoring electric vehicle trends in freight. This shift is primarily influenced by total cost of ownership (TCO) advantages and tighter regulatory pressures. Battery electric trucks are expected to surpass traditional internal combustion engines in TCO by 2025, boasting a 30% cost advantage by 2030. Significant investments will be required to expand infrastructure to support this rapid growth (Source: PwC Strategy& Report, view report).

- Consumer and Business Insights: A McKinsey & Company survey reveals that electric vehicle adoption varies significantly by region, with urban areas exhibiting higher purchase intent compared to rural settings. In particular, Germany shows a 30% intent for battery electric vehicles, while Italy leans towards PHEVs with a notable 41% intent. This report also stresses that while 93% of current EV owners express satisfaction with their vehicles, infrastructure gaps remain a critical barrier to wider adoption (Source: McKinsey & Company, view survey).

These statistics underline the ongoing transition towards electric trucks in the freight market, highlighting both the challenges and the substantial benefits, such as lower operating costs and compliance with emissions regulations, that are influencing fleet decisions amid fluctuating market conditions.

As the trucking industry is experiencing a significant transformation driven by the adoption of telematics and electric vehicles—crucial for improving operational efficiency and stabilizing market dynamics—stakeholders must emphasize sustainability in logistics. The following statistics reflect current trends in user adoption:

- Telematics Usage: The American Transportation Research Institute (ATRI) reports that telematics is now deployed in 89% of trucking fleets, increasing from 76% in 2020. The data also indicates that fleets adopting these systems achieve an average reduction of 13.2% in fuel consumption and a 15.7% improvement in asset utilization, helping them navigate market volatility efficiently (Source: ATRI).

- Electric Truck Adoption: According to McKinsey & Company, electric trucks are projected to constitute 30% of new truck sales by 2030, a significant rise from the current adoption rate of approximately 2%. This shift is expected to lower operating costs by 25-40%, creating a buffer against volatile fuel prices (Source: McKinsey).

- AI and Telematics: Advanced telematics that incorporate AI-driven analytics result in operational efficiency improvements ranging from 18-22%, according to reports from Transport Topics. Fleets utilizing predictive maintenance can reduce breakdowns by 45%, further enhancing reliability and addressing uncertainty in delivery schedules (Source: Transport Topics).

- Market Growth: The North American commercial telematics market was valued at 14.2 million units in 2023, with an 18% growth rate reported by Berg Insight. Fleets employing comprehensive telematics solutions not only see a 14.8% increase in fuel economy but also a 22% decrease in insurance claims, thereby providing added financial stability amidst changing economic conditions (Source: Berg Insight).

- Infrastructure Developments: CALSTART notes that over 12,000 medium- and heavy-duty electric trucks have been deployed in the U.S., reflecting a 140% year-over-year growth. Early adopters are seeing maintenance costs cut by 30-50%, which aids in mitigating fluctuations in operational expenses due to diesel price variation (Source: CALSTART).

These insights underline the critical role that telematics and electric vehicle technologies play in shaping a more resilient and efficient trucking industry. As fleets continue to adopt these technologies, they will not only improve their operational metrics but also stabilize their responses to market uncertainties.

Innovations in the Freight Market

The freight market is undergoing significant transformation thanks to innovations such as battery-electric trucks and fuel cell technology. These advancements position the industry to better address historical uncertainties related to fuel prices, emissions regulations, and overall operational efficiency while emphasizing sustainability in logistics.

Battery-electric trucks are becoming a cornerstone in the quest for sustainable freight solutions. Leading companies like Tesla are pioneering this shift, with the anticipated release of their battery-electric truck. This vehicle aims not only to reduce greenhouse gas emissions but also offers lower operating costs over time due to decreased fuel expenses and maintenance needs. The reduced complexity of electric drivetrains enables operators to achieve efficient logistics operations without succumbing to the volatility associated with fossil fuels.

On the other hand, fuel cell technology presents a compelling alternative, especially for long-haul freight. Vehicles powered by hydrogen fuel cells can provide longer ranges and quicker refueling times compared to fully electric trucks, making them ideal for routes that demand extended travel distances. Companies such as Nikola and Hyundai are making strides in developing hydrogen fuel cell trucks, emphasizing the versatility these vehicles offer in the ever-competitive freight market.

Moreover, the integration of these innovative technologies aligns with a growing emphasis on reducing carbon footprints. Changing regulatory landscapes favor cleaner operational practices which in turn incentivizes the use of environmentally friendly trucks. Government policies and subsidies aimed at enhancing charging infrastructure and hydrogen refueling stations foster quicker adoption of these technologies, encouraging freight operators to transition from traditional diesel-powered trucks.

The shift toward battery-electric and fuel cell vehicles signifies a broader commitment to sustainability within the freight sector. Embracing these innovations will not only help stabilize costs – by mitigating the impacts of fluctuating fuel prices – but also contribute to a cleaner environment, positioning the industry favorably for future challenges.

The review of the article indicated a detailed assessment of its structure, with observations highlighting potential repetition. The user adoption data related to electric trucks was presented in two distinct sections: one outlined as a summarized list and another section that provided a more detailed analysis. This could lead to confusion for readers, so one of these sections may need to be streamlined or consolidated to ensure clarity.

The historical fuel price changes were effectively summarized in a table, which enhances the readability and provides a clear visual reference for the readers. Additionally, there is a mention of a line graph in the text that shows fuel price fluctuations, but a proper link to the graph’s image was recommended to be integrated correctly into the document.

In terms of graphs, tables, and significant images, the review confirms there is only one existing table and one image placeholder related to the content presented. Therefore, it appears that no additional tables, graphs, or images need to be included unless new relevant data arises. The overall organization of information is generally clear, although slight adjustments may enhance reader engagement and understanding.